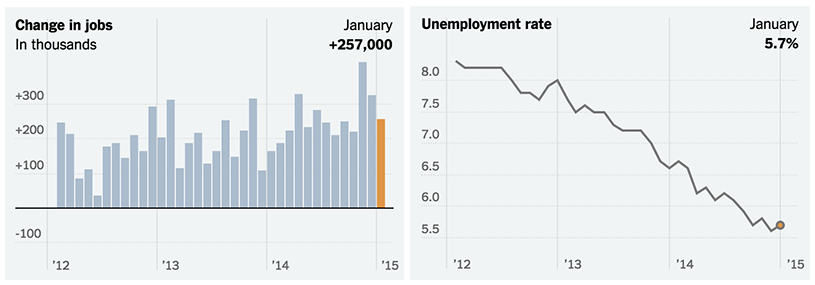

It looks like the economic momentum from the end of last year has carried over into 2015. According to the Labor Department, American employers added 257,000 jobs in January, with average hourly earnings increasing by 0.5 percent, the largest monthly gain in more than six years.

Despite the unemployment rate increasing slightly from 5.6 percent to 5.7 percent, economists still regard this report with optimism. “This is the best employment report we’ve seen in a long time,” remarked Guy Berger, U.S. economist at RBS Securities. “The labor market looks like it’s in really good shape as we head into 2015.”

The small increase in the unemployment rate was even considered good news, seeing as this fluctuation was primarily due to the increase in Americans actively looking for work rather than sitting on their couch.

Source: The New York Times via the Bureau of Labor Statistics

Spirits are so high after this report that the Fed is even considering raising short-term interest rates starting in June—a move that was originally expected to be delayed until September due to an assumption that inflation rates wouldn’t be where they needed to be.

“I still think it will be September, but the odds of a June increase have gone up somewhat,” Mr. Berger added. “The fact that the economy didn’t lose a step in January bolsters the case that inflation could hit the Fed’s target.”

And the Down Side…

Because there always is one. According to Steve Goldstein of Market Watch, we shouldn’t get too far ahead of ourselves. He claims that the surge in economic productivity we’re experiencing now is simply a playing out of trends we saw around this time last year, not to mention the product of an older, retiring generation of Americans driving up competition for new workers. In short, this economic growth isn’t groundbreaking—more just something that’s been a long time coming.

Goldstein also points out that the labor market is often an inaccurate indicator of economic productivity (a statement that we at GenFKD second). He cites the year 2007, when the U.S. entered a recession while simultaneously adding 99,000 new jobs (a seven-month high at the time). Conversely, 502,000 jobs were lost when the U.S. officially exited the same recession in June 2009. Basically, the labor market and monthly jobs reports are only a small slice of the economic pie—one that people tend to take a big bite out of.

What This Means for You

For starters, your chance of getting a raise rose by 0.5 percent, beating out most economists’ predications! *cue dancing sharks* To give you some context, payroll gains were $30,000 more than what was predicted, topping out at $257,000 total. This comes as a much needed boost after the December 2014 jobs report.

Albeit small, this is a step in the right direction in closing the devastating gap between what we owe in student loans and what we earn—a gap that is hindering college graduates from moving out, buying a house, buying a car and starting a family. The glaring absence of these often expensive adult milestones isn’t helping out our economy, either. But hey, if the student loan crisis isn’t going to be appropriately addressed, I guess there’s always shamelessly praying for payroll increases?

Seriously. One of these months I want to write “BOOM” in MS Paint. pic.twitter.com/qJIu4ONYdt

— Nick Bunker (@nick_bunker) February 6, 2015

We feel you, Nick.

Head on over to the New York Times for the full break down.