401(k) noun ˌfȯr-(ˌ)ō-(ˌ)wən-ˈkā:

Definition: a contribution plan where an employee can make contributions from their paycheck either before or after-tax, depending on the options offered in the plan. The contributions are filtered into an account & expand over time due to interest.

For those of you that inexplicably picture gray haired yuppies & yachts at the mere mention of this mysterious number-letter combination – close, but no cigar.

401(k)s are not just for wealthy old people.

If that’s not news to you, excellent. If it comes as a slight shock, I’m right there with you.

The truth: many of the most financially successful humans you know owe much of their fiscal stability to their 401(k) plan. Thankfully, you don’t have to wait to follow their lead. The sooner you begin saving, the more earning potential you have.

Sound boring enough? I feel you. I’ll keep it short & sweet.

Reasons You Don’t Care About 401(k)’s:

“No need to worry yet.”

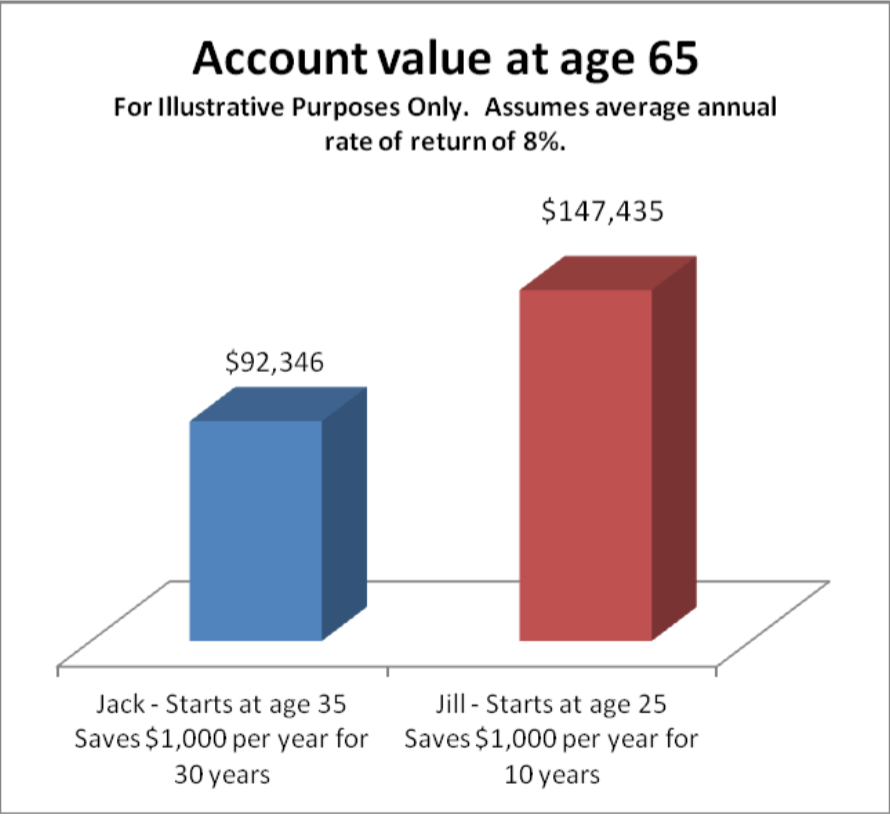

The world will continue to turn if you delay starting a 401(k). These plans will still be available when you turn 30 and your survival doesn’t depend on enrolling in one. However, if you want to acquire the most possible money from a 401(k) by the time you hit retirement age (or in general), then there’s no time like the present. Even if you plan to take extended time off from working (to raise children, travel the world, start your own business etc.), the money you initially move into your 401(k) will continue to earn income. A 401(k) relies on a positive rate of investment return to help you begin growing your wealth. The most powerful leverage you have over this benefit is time.

“I plan on changing companies soon, anyway.”

For many millennials, the idea of a traditional lifetime career is a foreign concept. Many of us are more focused on individual professional growth rather than maintaining a long-term commitment to a specific company. That said, recent studies show that millennial job-hopping is not necessarily a unique occurrence. Throughout history, 22- to 29-year-olds have been susceptible to frequent career changes.

This is not a reason to avoid saving. Just like your laptop, 401(k)’s are portable. If you decide to move to another company that also offers a 401(k), you will generally have the option to rollover your money into your new company’s 401(k) Plan or, if your balance is at least $5,000, let it remain in your former employer’s 401(k). Similarly, if your new company does not offer a 401(k), you also have the option to easily rollover your money into an IRA (Individual Retirement Account).

If you have less than $5,000 in your 401(k) when you leave a company, they may force you to move your funds. However, they cannot require you to move those funds by cashing out. Here’s a hint: don’t! If you are under the age of 55, withdrawals from 401(k)’s are subject to income tax and a 10 percent early withdrawal penalty. Rollover instead!

“I don’t work for a company that offers a 401(k) plan.”

While you may not have an opportunity to begin a 401(k) yet, educating yourself about the benefits, potential risks and maintenance of a 401(k) will make all the difference when the time comes for you to invest in your future.

Plus, even if you do not currently have the opportunity to start a 401(k), you’re not necessarily out of luck. Many 401(k) plans allow you to rollover from an IRA, so you may be able to join in the fun sooner than you think!

“I don’t make that much. Why would I lessen my paycheck?”

In the short run, you’ll be reducing your spending money by filtering a portion of your paychecks into a 401(k). That said, the benefits of a 401(k) are not exclusively long-term. 401(k)’s are not only great for growing wealth, they’re also a tax shelter. Funds contained within a 401(k) plan are not taxed. An even cooler fact: because your income subject to taxes will be reduced, your taxes will be reduced as well!

“Is that all?”

Nope, there’s more. Most companies that have 401(k) plans will give matching contributions to employees who participate. For example, a company sponsor may, for every $1 put into the 401(k), match $0.50 up to a percentage limit (6 percent of compensation). So, if a person with this plan makes $2,000 per month and puts 10 percent ($200) into their 401(k) each month, that company will put another $60 in each month (lesser of 50 percent of $200 ($100) and 3 percent of $2000 ($60)). The percentages vary by employer, but many plans offer this added benefit!

If you decide to join the 401(k) club, just know: there’s a cardigan-wearing, smooth-sailing retirement out there with your name on it.

Still somewhat apathetic about 401(k) plans? You’re not alone. Share your concerns in the comments below, or check out our Facebook page.

Compliance Statement: The content is developed from sources believed to be providing accurate information. The information in this material is not intended as tax or legal advice. Please consult legal or tax professionals for specific information regarding your individual situation. The opinions in this blog are not representations of the company by which I am employed.